Q4 ‘21 – an All-Time High

After continuously breaking funding records throughout 2021, the Israeli ecosystem delivered on its funding streak in Q4, bringing the total funding of 2021 to a new peak of $27B – more than doubling the amount raised in 2020.

Not only did the momentum continue, but Q4 actually broke records even for this record-breaking year, with $8.1B in funding, which is almost a ⅓ of the year’s overall funding. This makes Q4 of ‘21 to an all-time high in funding.

Beyond Security and FinTech – Investments Breakdown

When looking at leading sectors in the Israeli ecosystem in terms of funding activity, Security and FinTech are naturally the immediate suspects. This has continued throughout 2021, when these 2 categories were responsible for 42% of the overall funding. Both have shown growth, with Security rising from 21% of overall funding to 25%, and FinTech growing from 15.5% to 17%. With the acceleration in digital transformation, the workforce moving to remote/hybrid, shopping moving to e-commerce etc, these two sectors will continue to see a significant boost.

However, the ecosystem growth doesn’t stop here. Israeli companies showed significant funding versatility, with more sectors stepping into the spotlight, including: IT/DevOps (Redis Labs, RapidAPI, OwnBackup, Atera Networks), RetailTech (Trigo, Bringg, Trax, Fabric, Yotpo), Sales and Marketing (Gong, Lusha), Healthcare (Immunai, K Health) and Semiconductors (Speedata, ProteanTecs, Wiliot, Hailo, NextSilicon), driven by the exponential growth in data and digital consumption.

Early Stage Stays Stable, Mega Rounds Explode

When looking at the investment breakdown by stages, Israel is aligned with global trends: Early stage funding stayed stable, but median deal size increased by more than 50%- from $4.1M to $6.3. This may be driven by the asymmetry between the infinite supply of dry powder and the decreasing number of new startups founded, resulting in the reduced number of early stage rounds (from 1145 in 2018 to 954 in 2021).

On the other hand, Growth (>$30M) and Mega (>$100M) rounds have seen explosive growth – not only in size but also in pace. The number of Mega rounds jumped from 21 to 79 In one single year.

Pre-Money Valuation Are Exploding in Growth Stage

It’s interesting to see how this translates into the pre-money valuation of Israeli companies – while early stage deals valuations are on a steady increase, Mega rounds valuations are exploding.

Q4 2021: From Startup Nation to Unicorn Capital

Unicorns have been known to thrive in the Israeli ecosystem for some time now, and yet, 2021 may be THE year Start Up Nation has finally become the unicorn capital of the world, second only to the US in terms of new unicorns last year. While Israel’s startup funding stands at the 5th place in the world at $27B, it has surpassed the UK, India and even China with 48 new unicorns – and follows the US, which has 314 unicorns and also leads with $330B in funding.

When it comes to unicorns per capita, though, Israel unequivocally leads at 5.2, with Singapore following from afar at 1.8 and the US at 1.

ACROSS VERTICALS, ACROSS BUSINESS MODELS

One thing is certain – Israel is not a “one trick pony”. Israel’s billion Dollar companies are present across numerous verticals and business models, from Consumer to FinTech, Infrastructure, Security, and Vertical Applications. While some categories are more traditionally dominant in the Israeli ecosystem, some are new to the unicorn category, such as Vertical Application (Verbit, Immunai, Bringg) and Horizontal Applications (Papaya Global, Lusha).

2021 Unicorn Cohort Make Up ~60% of the Total Number in Each Category

Beyond the impressive number of companies that reached unicorn status in 2021, it’s important to note how many of these new unicorns have led to category growth. For example, 9 out of the 15 Israeli unicorns in the Security sector reached the billion Dollar valuation in 2021. The same is true for Vertical Applications – out of the 12 unicorns in this category, 8 were “born” in 2021. And it doesn’t stop there.

REACHING HIGHER VALUATIONS WHILE PRIVATE

Not only do we see more companies reaching unicorn status (3X from 2020), but they are surpassing it, while still staying private, with 7 companies reaching a valuation of over $7B in 2021.

Time to Unicorn

We continue to see acceleration in the pace of reaching unicorn status, with companies reaching the $B valuation in less than 2-5 years. For example: in 2018 there were 8 companies that reached unicorn valuation in less than 5 years.

Q4 2021: M&A and IPOs Breaking the Mold

2021 was a significant year for both M&As and IPOs in the Israeli ecosystem, showcasing the ecosystem’s maturity as well as recovery from the pandemic. Speaking of recovery, Israeli M&As bounced back from the dip they experienced in 2020 (with 110 exits compared to 2019’s 147) with no less than 153 M&As.

Some notable M&As include MyHeritage (acquired by Francisco Partners), Guardicore (acquired by Akamai), Chorus (acquired by zoominfo), Espagon (acquired by Cisco), and DSP Group (acquired by Synaptics) – each of them acquired for over $500M each.

From $9B to $84B in Market Cap in Public Debut

But M&As weren’t the only liquidity events in 2021. Last year broke all records of Israeli companies making their public debut, with an astounding leapfrog from $9B to $84B in market cap. SPACs continued to be all the rage (after coming back to popularity in 2020), with 12 out of the 25 IPOs held in US public markets consisting of SPAC deals.

A Year of Non-Organic Growth

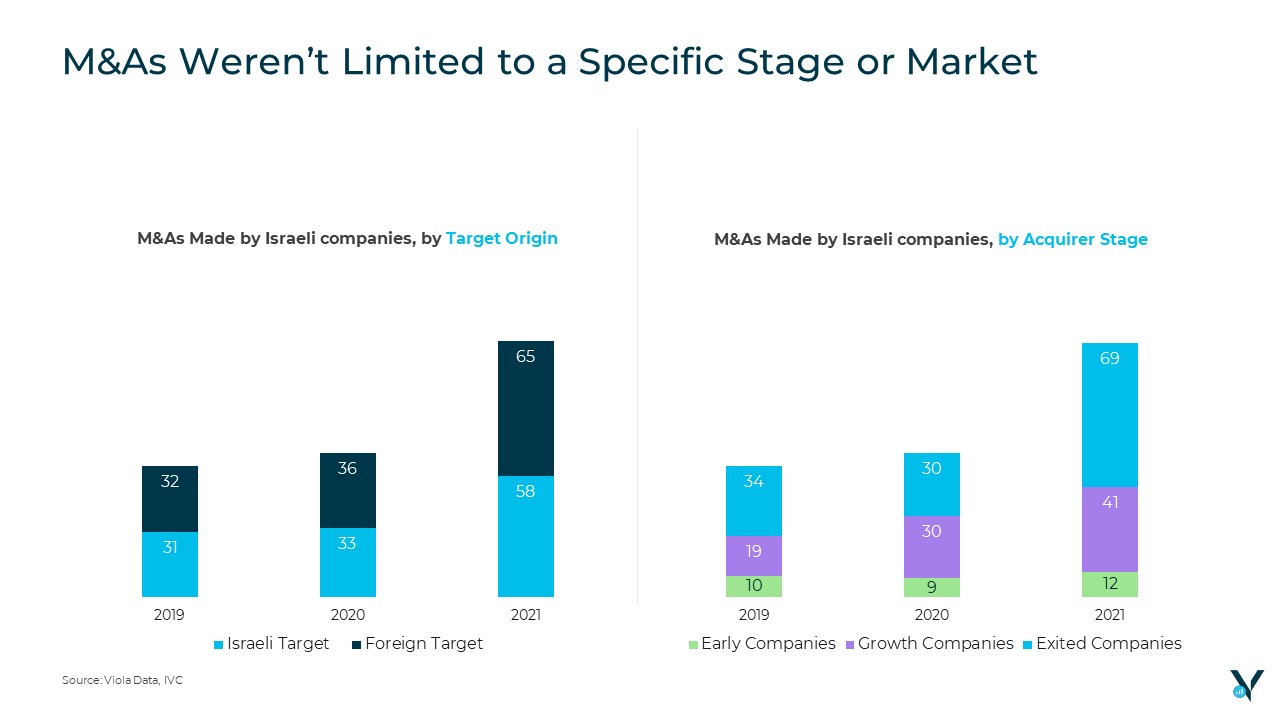

A newer phenomenon which was noticeable in 2021, was Israeli companies participating in M&As as the acquirer. M&As made by Israeli companies soared by 56%, as a tool for non-organic growth. Some, like ironSource and Bizzabo made 4 acquisitions each, in a single year.

With tech companies raising more capital than ever, and valuations being driven by growth rates, we expect this phenomenon to accelerate as companies deploy capital to foster growth and expand market share. Interesting to see that these M&A happened across stages and markets, with no less than 12 of the acquirers being early stage companies.

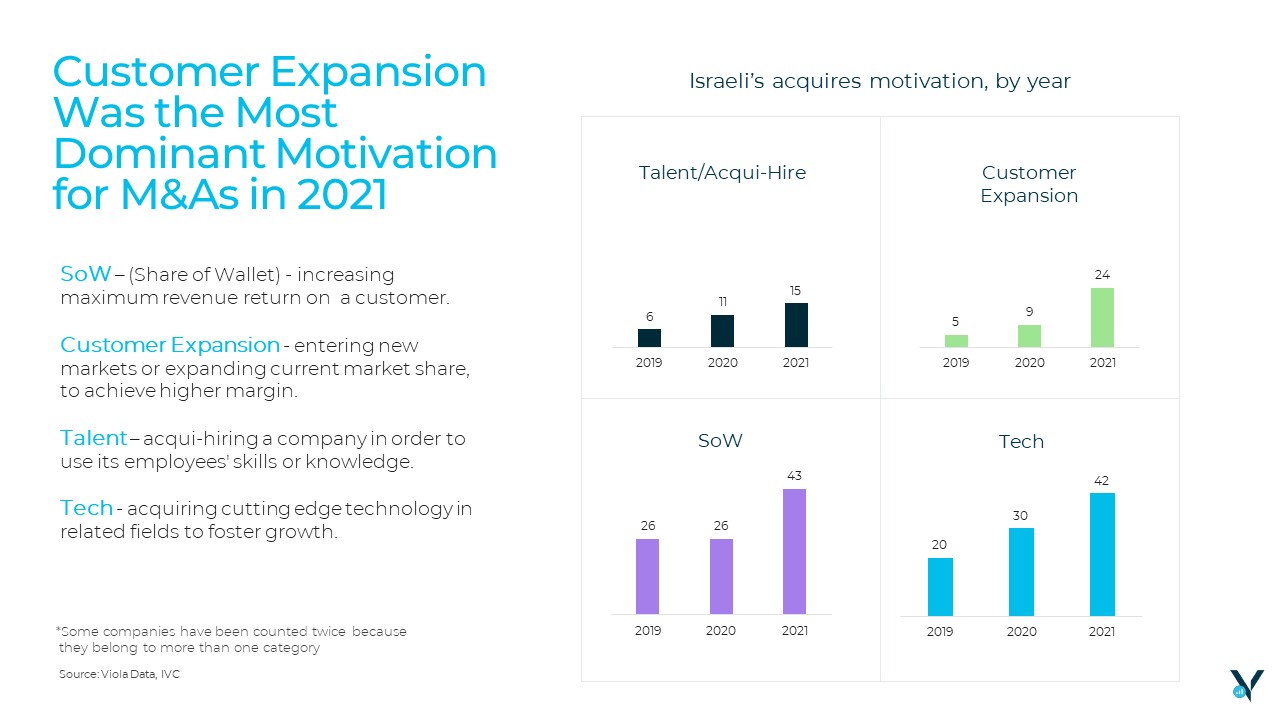

Diving into the motivation behind these acquisitions, one can see that they varied from increasing share of wallet to acquiring talent and technology. However, the most dominant motivation was customer expansion. Many companies either acquired smaller companies in their existing market or entered new markets in which they can benefit from existing technology, and improve their margins.