The Mobility market has undergone major technological disruption in recent years. Propelled by innovation, it is driven by the primary goal of reducing the cost of transportation (per mile per person/package) through the all-important trinity of Shared, Autonomous and Electric vehicles (SAEVs). A race is now underway to lead the fulfillment of this future mobility dream, and leverage cost reductions to introduce innovative, on-demand services to businesses as well as consumers.

With the first wave of Israeli mobility startups now at its peak and dedicated mainly to In-Vehicle and Mobility Services technologies, we anticipate that the next wave will focus on solutions connecting the vehicle to its environment and introduce mobility services that leverage new innovative technologies.

We have embarked on a mission to analyze, categorize and map the local mobility landscape, and are pleased to share our findings.

The 3 Main Layers of Mobility

We segmented mobility-related companies into 3 main layers sharing common characteristics in the value chain:

1. In-Vehicle

This layer includes technologies implemented inside vehicles, and are typically sold to OEMs, Tier 1’s and potentially to new entries such as Waymo, Baidu and Uber. Contracts in this layer are commonly significant and categorized by lengthy periods of design, specs, integration and more. Israel has excelled in this area, with several significant companies (e.g. Mobileye, Innoviz and Valens) which have developed high caliber, multidisciplinary technologies and succeeded in closing significant deals with car manufacturers. We believe that this area will continue to develop in the local ecosystem.

2. Connectivity & Operational Interface

Even when equipped with a wide variety of in-vehicle technologies – SAEVs cannot exist in a vacuum. A scalable, secure SAEV operation will require complementary connectivity and operational solutions in the interface between the vehicle and its environment. For example: Massive proliferation of autonomous vehicles (AV) will require supporting city infrastructure, stable, high-speed communication and robust cybersecurity, and electric vehicles (EV) will require infrastructure with adequate power supply and distribution capabilities – all of which will enable precise large-fleet orchestration with zero downtime tolerance, loss of control or other safety issues.

3. Mobility Services

This layer is focused mainly on the fields of consumer, fleet management, ride hailing and logistics. Just as the first wave of mobility leveraged the new technologies of its day (namely smartphones and AI) to introduce new services – creating significant companies, such as Moovit, Gett and Via – we anticipate the next wave will take advantage of new SAEV technologies (such as cars connected to each other and the surrounding infrastructure) to “upgrade” our experience and introduce more effective ways of performing a variety of tasks.

We believe that as it develops, we will see more innovation in physical platforms and better compatibility between tasks and the platforms responsible for performing them. For example, rather than using a standard car for a pizza delivery, the task might be performed by a droid (a small type of robot) whose size and mass are better suited to the item being delivered. The inevitable (and dramatic) decrease in the cost of transportation and delivery time we will see as a result, will give rise to a whole new world of B2B and B2C services, and additional “winners” will emerge in this space.

Israel’s Mobility Landscape

Selection criteria for inclusion in the map: Innovative Israeli or Israeli related companies that offer solutions to the mobility industry. NOTE: The map is updated on an ongoing basis (refer to the version number at the bottom to ensure you have the latest one).

[Click to enlarge/download]

Notable insights about the Israeli Mobility Landscape

![]() More Mobility startups than ever.

More Mobility startups than ever.

Israel’s mobility landscape has grown immensely in recent years. Between 2014-2018, the number of mobility startups founded grew by virtually 100% vs. 2009-13, with the peak year being 2016, accounting for 27 companies founded.

Google’s acquisition of Waze in mid-2013 for a record $1.2B and Mobileye’s $5.4B blockbuster IPO the following year, marked a turning point for the local ecosystem, only to be surpassed 3 years later by Mobileye’s taking private by Intel for an astounding $15.4B (the largest Israeli technology acquisition to date) – all seem to have drawn the attention of Israeli entrepreneurs, giving rise to an active and fruitful ecosystem.

![]() Median funding rounds have grown by over 100% YoY.

Median funding rounds have grown by over 100% YoY.

The majority of the Israeli mobility companies we have identified require ongoing venture funding. Total money raised has grown from about $180M in 2015, with a median deal size of less than $3M, to $730M in 2017 with a median deal size of $6M. Though median deal size has grown to $10M, total funding in 2018 has been sub-$400M to date, with no mega-deals such as those we’ve witnessed in recent years. However, with leading mobility startups currently fundraising large sums, we expect this number will grow significantly by the end of the year (chart 1).

![]() Only a handful of companies raised the lion’s share of total capital invested.

Only a handful of companies raised the lion’s share of total capital invested.

Israel’s mobility companies have raised roughly $5B. As funding rounds are often unannounced, it’s reasonable to assume that the actual funding figures are 15-20% higher. Leading the table is Mobileye, which raised over $2.3B just on its own (including public offerings); and the top half dozen outliers account for more than three quarters of the total funding.

![]() Significant number of companies have reached growth funding rounds

Significant number of companies have reached growth funding rounds

Considering the funding stage of local mobility companies, we see a distribution typical of a growing market, with early companies entering alongside numerous companies reaching growth funding rounds, and completing the cycle, there is a significant percentage of companies reaching liquidity – all indicative of high demand for technologies and products (chart 2).

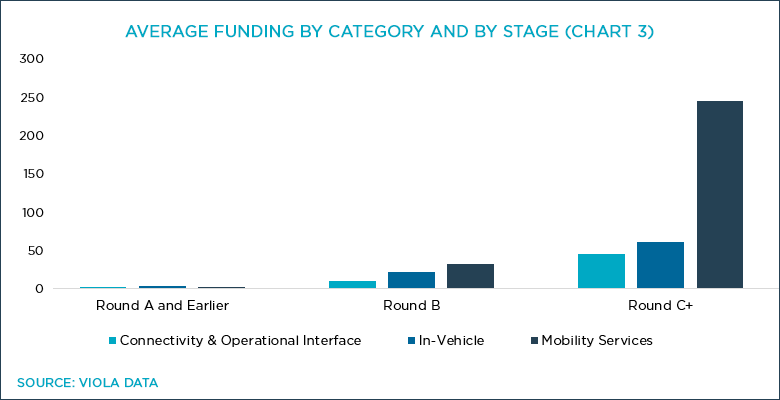

![]() Mobility Services startups require more capital.

Mobility Services startups require more capital.

Growth stage Companies in the Mobility Services space have raised on average more than three times the capital than mobility companies from the other ‘layers’, and double if excluding outliers, such as Gett and Via which have raised hundreds of millions of dollars each (chart 3).

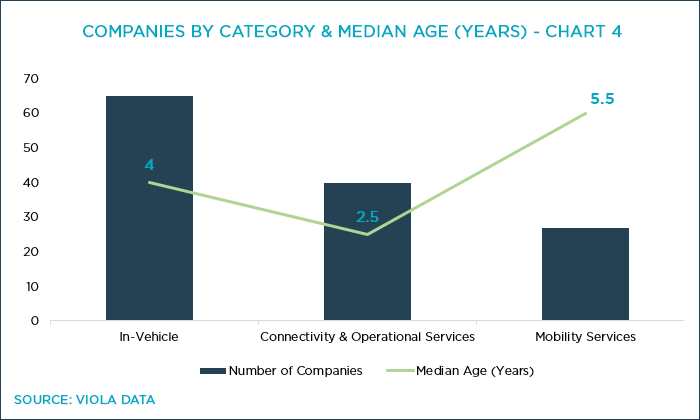

![]() Connectivity & Operational Interface is the youngest ‘layer’

Connectivity & Operational Interface is the youngest ‘layer’

The Connectivity & Operational layer includes 40 companies with a median age of only 2.5 years. Rich with new technologies and innovation, we believe this vertical will play a major role in creating future local mobility success stories (chart 4).

![]() Exits have ramped up since 2015

Exits have ramped up since 2015

Of the 11 exits in the space, 8 took place since 2015, 5 were in the Connectivity & Operational Interface space and 4 in the In-Vehicle space. It’s worth noting that of the 11 companies acquired, 3 thus far were by a single acquirer, Harman International Industries (Red Bend, Towersec and iOnRoad).

FINAL THOUGHT: With dramatic announcements by both OEMs (such as Ford, which plans to operate its own robo-taxi network by 2021) and governments (like California’s, which aims to reach 5 million zero-emission vehicles on its roads by 2030) – it’s clear the demand for innovation in mobility will increase in coming years. More Israeli mobility companies are being founded, more capital being raised and global recognition by international players investing and acquiring companies – all pointing to the fact that the Israel’s Mobility industry is not only here to stay, but also to grow.

More Israeli mobility companies are being founded, more capital being raised and global recognition by international players investing and acquiring companies – all pointing to the fact that the Israel’s Mobility industry is not only here to stay, but also to grow.

|

Know of a company that should be added Email us at: mobility [at] viola-group [dot] com |