As we wrap up the first half of 2023, we continue to track the volatility in tech investments and analyze the Israeli ecosystem’s standing as compared to global tech. While this rollercoaster is still very much in effect, we see it reflected in the numbers – but also find reasons for optimism.

Investments in Israel have Dropped Further than Globally

Investments have continued to drop globally in H1, with $168B compared to $333B in H1 of 2022 and $348B in H1 of 2021. This represents a 50% YoY drop.

In Israel, investments have also dropped below 2018-2020 numbers with $3.2B in published investments. More importantly, though, this number represents a YoY drop of 73% from H1 2022’s $12B.

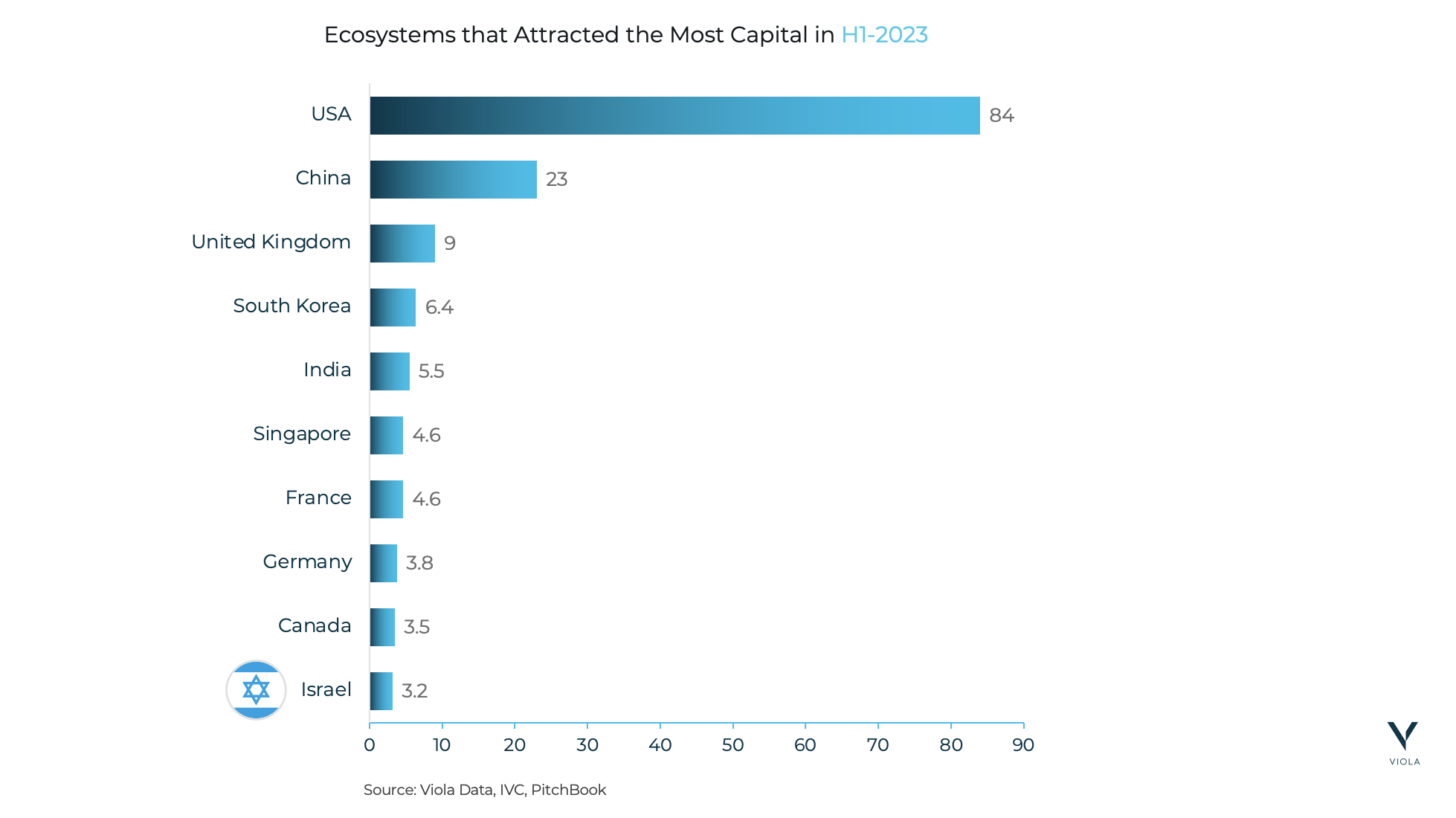

Until now, Israel managed to maintain its place as the 5th largest tech ecosystem in terms of funding, but due to the sharp decline in 2022-3, it dropped to 10th place, below South Korea, Singapore, France, Germany, and Canada.

Reasons for the Dramatic Decline:

The entire tech industry is feeling the impact of the economic downturn, but the Israeli ecosystem had some unique circumstances affecting it – some of them may lend some optimism:

1. A Higher Tide Leads to a Lower Ebb

The last five years have seen some dramatic ebbs and flows in the capital invested in tech, worldwide. But while global investments increased by 108% from H1/2018 to H1/2021, the Israeli number for the same period was no less than a 250% increase. With a peak that’s more than double, the corresponding drop seems more pronounced, but still not at the same rate.

2. Larger Rounds, Longer Runways –

2. Larger Rounds, Longer Runways –

During Q1 and Q2 of 2022, Israeli startups have consistently raised more than their global peers. While the global median for Seed-A rounds in Q1 and Q2 was $3M and $3.1M (respectively), the Israeli median was $5M in Q1 and $6M in Q2, for the same stages. When it comes to B to D rounds, there is a clear gap as well, especially in Q2 of 2022. In Q1 of 2022, the global median was $35M, while the Israeli median was $37.5M. In Q2, this gap grew – with a global median of $30M, compared to an Israeli median of $38M.

With these amounts of investment, many Israeli startups have longer runways, hence less need of raising investment in H1 of 2023.

3. Political unrest – around the judicial reform could be a contributing factor to certain investors who are concerned about potential uncertainty. The Israeli tech ecosystem is working diligently to find a bi-partisan, wide consensus resolution.

Room for Optimism – What’s Next?

- A Look at Extension Rounds Hints that Total Funding is Higher:

While brand-new rounds were rarer than usual, extension rounds reigned supreme this year, representing over a third of H1’s published rounds. We believe that the actual amount of extension rounds is even higher.

Many startups chose not to publicize these extension rounds in order to avoid negative perceptions. Due to the economic environment, many other rounds are formed as SAFE rounds, which are not reported as investment rounds, and are not included in the total number of investments. Therefore, we believe that the actual total amount of investment is more positive than what reported numbers can lead us to think.

2. Israeli Public Companies are Keeping Up with US Performance:

The drop in new investments may be concerning, but ITI companies – the 31 Israeli public tech companies included in Viola’s Israeli Tech Index – are doing well. Looking at the last 3, 6, and 18 months, ITI companies are showing performance that is consistently in line with EMCLOUD companies, ׂthe Nasdaq’s emerging cloud indexׁ). And it’s constantly improving. This shows that the market’s sentiment for Israeli public companies is similar to its sentiment for US public companies.

3. New Frontiers for Start-Up Nation:

The tech industry upheaval is definitely shaking things up, and for some verticals – this may be good news. While the first wave of Start-Up Nation was born out of the volatile situation following the Dot Com burst in 2000-2001, and many of today’s Scale Up giants were first founded following the 2008 crisis, we see signals for a new wave of meaningful, breakthrough innovation. We believe the next big transformative tech companies are born now, on the waves of this new innovation cycle driven by AI-everything in sectors such as ClimaTech and Digital Transformation.

Investment Across Stages – A Closer Look

As previously mentioned, total funding activity in Israel has decreased by about 70% from H1 of 2022, while the decrease varies across the board. Let’s take a closer look at the different stages and how the current situation has affected investments:

Mega Rounds –

This stage is the one that’s seen the most turbulence, with a steep decrease from the hype of 2021 which amounted to $8.2B in H2-21, to $1B in H1 of 2023. The number of deals has also dropped significantly from 41 at the very peak to 7 so far this year. There are many contributing reasons, but a notable one is the foreign investors who were uber-active in leading late-stage rounds in 2021, only to abandon ship in 2022 and this trend continued throughout H1-23.

Growth Rounds –

Growth stage investments have also continued to decrease, both in matters of deal size and deal number. In H1 of 2023, there have been 34 growth stage deals, compared to 51 in H2/2022 and 80 in H1/2022. The median deal size has also decreased from $50M in H1/2022 to $39M in H1/2023.

Early Rounds –

Early-stage investments were the last to be impacted, but the overall trend has now caught up with them, too. After H1/2022’s peak of $3.4B overall in early-stage investments (with a median deal size of $5.2M), we see $1.5B in projected capital in H1/2023 for this stage, with a median of $4M. According to our data projections, H1-23 will end with 350-400 early-stage rounds, compared to 602 in H1/2022 and 550-600 in H2 of the same year. We expect to see the trend continuing in the next quarter with fewer deals and lower investment amounts.

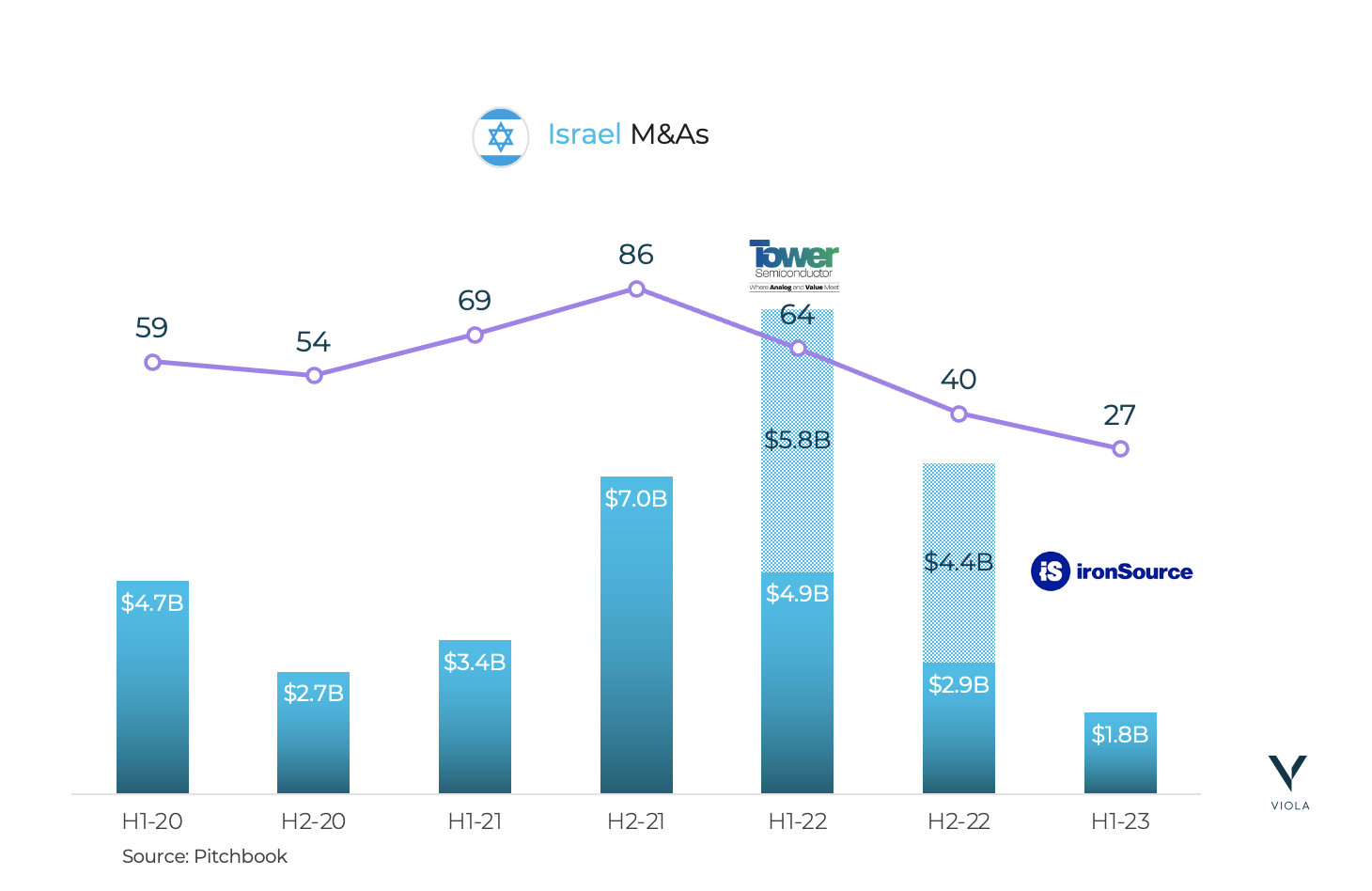

M&As – An Upcoming Wave On the Horizon

M&A activity in Israel has been pretty slow in H1. However, the M&A buzz in the ecosystem is palpable. There is a strong interest from all sides: startups exploring liquidation, and strategic corporates and PEs seeking opportunities and trying to scoop up attractive targets and bolstered deals while they are attractive. We believe that a wave of M&As will arrive in the next 12 months.

Finally, the Israeli ecosystem is definitely feeling the full impact of the downturn after years of a consistent high, yet it is keeping its seatbelt fastened through this intense rollercoaster.

We will continue to track and report as the situation evolves.