The first article in this series outlined the central tension of the AI economy. Trillions of dollars are being deployed to build the infrastructure of intelligence, yet the revenue layer required to justify that investment remains underdeveloped. The system is scaling, but its economic logic is not yet complete.

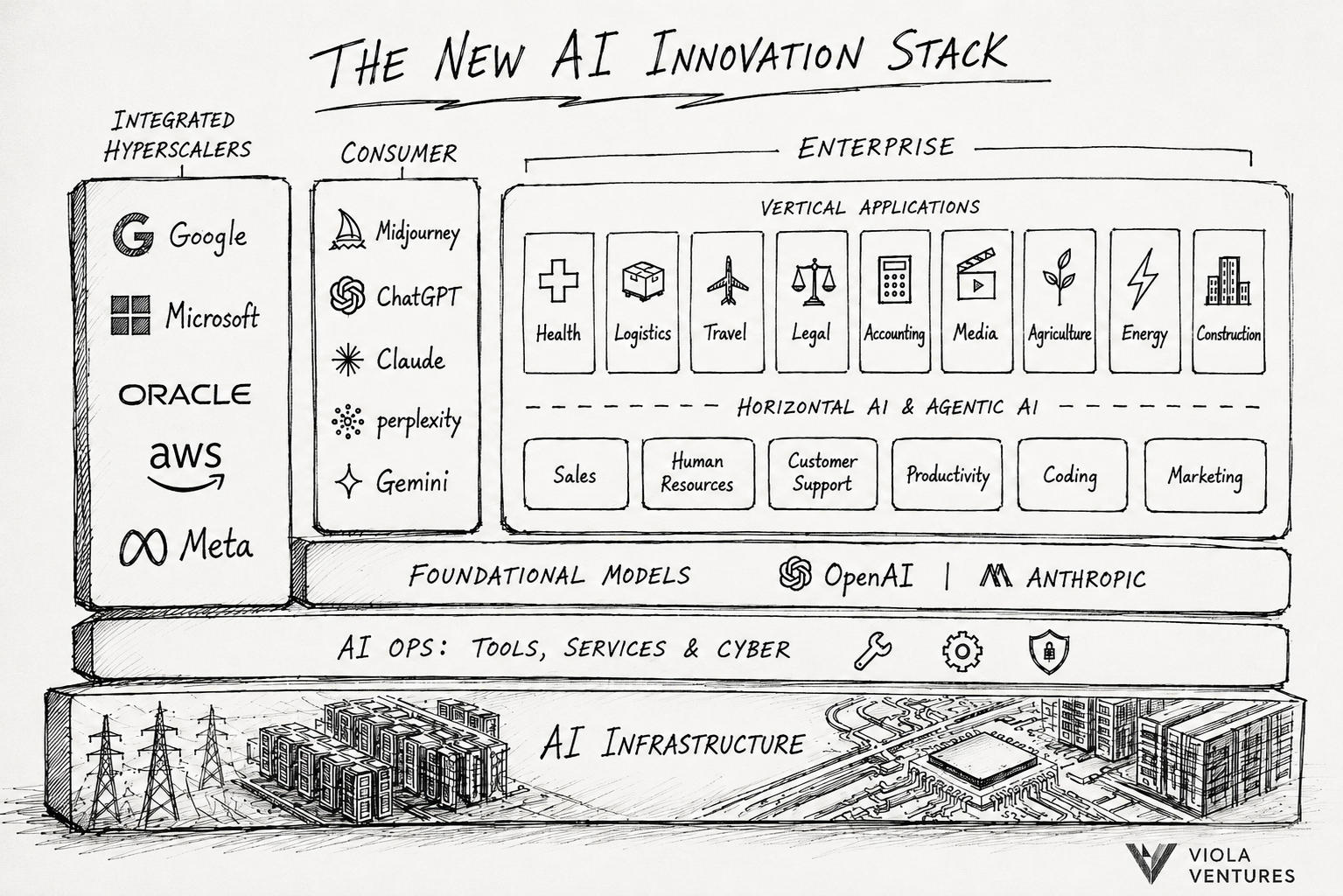

To understand where that logic might emerge, it is necessary to examine how the AI market itself is structured: What has taken shape over the past two years is not a single market, but a vertically layered system.

At its foundation sits AI infrastructure, a capital-intensive base of chips, data centers, networking, and energy systems, increasingly dominated by hyperscalers and a small number of hardware providers. Above it, a new operational layer is emerging, comprising tools that manage, optimize, and secure AI workloads. This includes orchestration systems, inference optimization, observability, and governance, all of which determine how efficiently compute resources are deployed and how safely they are integrated into real-world environments.

On top of these layers sit the foundational models themselves, which have captured the majority of attention and capital. The competition between OpenAI, Anthropic, Google, and others has defined the current phase of the market, with rapid improvements in capability and scale. These models have, in turn, enabled the fastest consumer adoption curve seen in modern software. Applications such as ChatGPT, Claude, and Gemini have reached hundreds of millions of users, establishing AI as a daily interface rather than a niche tool.

And yet, for all its speed, this layer has not produced commensurate economic depth.

Consumer AI has achieved scale, but not stability. Revenues across the category remain measured in the tens of billions of dollars annually, a figure that is meaningful in isolation but marginal relative to the infrastructure being built beneath it. More importantly, the structure of the consumer market limits its ability to generate durable value. Users move fluidly between models as performance converges, switching costs remain low, and differentiation erodes quickly as competitors close capability gaps. Distribution is increasingly controlled by hyperscalers, further compressing margins and reinforcing platform dependency.

This is reflected in how capital has been allocated. The majority of investment has flowed into foundational models and, adjacent to them, into developer tooling, particularly in coding. These categories are not without merit. Coding, in particular, offers clear and immediate productivity gains, which explains its massive traction. But they represent only a narrow slice of the broader software economy. Neither foundational models nor coding tools, in their current form, are sufficient to absorb the scale of capital being deployed into infrastructure.

This leaves a conspicuous gap at the top of the stack.

Historically, infrastructure of this magnitude has only been justified when a dominant enterprise layer emerged to convert technological capability into durable revenue. In the cloud era, that layer took the form of SaaS. Enterprise software systems became deeply embedded in workflows, generated recurring revenue, and exhibited high switching costs. The AI era has not yet produced an equivalent.

Incumbent enterprise software companies have moved quickly to incorporate AI, but largely through incremental additions. Copilots, assistants, and generative features have improved user interfaces and enhanced productivity, yet they have not fundamentally restructured enterprise workflows or created new, independent revenue pools. AI, in this context, remains additive rather than transformative.

Even Claude, arguably the company most singularly focused on enterprise API adoption, is still only at the very beginning of the curve. Anthropic reportedly crossed roughly $40B in revenue run-rate, driven largely by developers and enterprise customers, yet the market opportunity ahead remains dramatically larger.

At the same time, what is becoming increasingly visible in public markets is that the traditional SaaS model is showing signs of strain under this new paradigm. Salesforce, long considered the archetype of enterprise SaaS, trades at roughly 5–7× forward revenue, well below the double-digit multiples it commanded at its peak. Adobe, despite strong fundamentals, trades closer to 7–9× forward revenue, reflecting both macro compression and uncertainty around how generative AI will reshape its core businesses. Even best-in-class platforms such as ServiceNow, while still commanding a premium at approximately 13–16× forward revenue, have seen multiples normalize relative to the prior cycle.

Generative AI challenges several of the assumptions that underpinned SaaS economics. Software is no longer purely deterministic; it is becoming probabilistic and model-driven. Value is shifting away from static systems of record toward dynamic systems of execution. Interfaces are collapsing into conversational layers, reducing the importance of traditional application surfaces. And, critically, the cost base is changing: compute and inference introduce variable costs into what was historically a high-margin, near-zero-marginal-cost model. At the same time, incumbents face a strategic dilemma. Integrating AI into existing products is necessary to remain competitive, but doing so often bundles new functionality into existing pricing, rather than creating entirely new revenue streams. This risks increasing cost without a commensurate expansion in revenue, compressing margins over time.

This does not imply the disappearance of enterprise software. But it does suggest that the first generation of SaaS companies may not be the primary beneficiaries of the AI era. The characteristics that defined success in the cloud cycle: seat-based pricing, workflow digitization, and incremental feature expansion – may not translate directly into a world where software increasingly acts autonomously and outcomes replace interfaces.

In that sense, what is unfolding is not the death of SaaS (as many like to call it), but the end of SaaS as we have known it.

Claims that generative AI will “kill SaaS” are both premature and conceptually flawed. Software does not disappear when underlying technologies change; it reorganizes around new abstractions. Just as the cloud did not eliminate software, it redefined it – AI will do the same.

What is changing is not the existence of SaaS, but its economic and architectural foundations. The first generation of SaaS was built on systems of record, structured data, and deterministic workflows. Value was created through digitization, standardization, and interface design. In an AI-native world, value shifts toward systems that can reason, act, and adapt in real time. The unit of value is no longer the interface, but the outcome.

If software begins to own outcomes rather than workflows, pricing models, margins, and competitive dynamics all change. Seat-based pricing becomes less relevant when a system can replace labor rather than augment it. Margins become more variable when compute and inference costs scale with usage. Switching costs evolve when intelligence is portable across interfaces.

Yet none of this implies that SaaS disappears. Enterprises will still require systems to manage data, enforce workflows, ensure compliance, and integrate across functions. In fact, as AI introduces more variability and autonomy into operations, the need for reliable, structured systems may increase rather than decline.

What changes is where value accrues. The winners of the next cycle will not simply be those who add AI features to existing products, but those who rebuild enterprise software around AI-native primitives. The mistake is to confuse disruption of incumbents with destruction of the category – SaaS is not dying, it is simply being rewritten.

The mistake is to confuse disruption of incumbents with destruction of the category – SaaS is not dying, it is simply being rewritten. And until such a layer emerges, the AI stack remains structurally incomplete. This is the core of the two-trillion-dollar problem. Infrastructure is being built on an industrial scale. Models are advancing rapidly. Consumer adoption is widespread. But the economic center of gravity, the layer capable of absorbing cost and generating durable returns, has not yet taken shape. And yet, this gap is precisely where the opportunity lies.

As a seed investor, I am cautiously optimistic. The absence of a fully realized enterprise layer suggests that the most important phase of the AI economy is still ahead.

If AI follows the pattern of previous infrastructure cycles, value will ultimately accrue not to the layers most visible today, but to those that embed themselves most deeply in the operations of the real economy.